The public must confront and understand the forces that drive global oil markets if we are to move beyond nonsensical and counterproductive reactions to higher pump prices.

By Ryan McGreal

Published February 28, 2011

I have read the mainstream media coverage of the past week's run-up in oil prices with steadily mounting frustration.

The price per barrel of oil drifted around the $80 mark for a year, but spiked last week to over $100 and triggered the usual litany of media reports about pump prices and irate motorists.

A Spectator editorial on Saturday made some noises about Libya and concluded, "there is no logical reason for the Libyan crisis to have the impact it has. This is about fear and speculation."

Noting that Libya only produces 2% of the world's oil and that production hasn't stopped during the recent civil uprising, the Spec blames investors "betting on worst case scenarios" in the Middle East for the oil price spike.

Left unasked are any questions about why the mere possibility of a 2% drop in global oil production would trigger such a panic. It's eay to blame speculators, but why are these investors so willing to bet on volatility in the first place?

Why, for that matter, was oil trading as high as $80 a barrel througout last year, a year the world was supposed to be just crawling out of a sharp recession?

The attempt to answer these questions leads to deeper questions about the forces that have been driving oil markets over the past several years - questions the public must confront and understand if we are to move beyond nonsensical and counterproductive reactions to higher pump prices for our gasoline.

It may seem unlikely that a modest drop in output - or even the threat of such a drop - could translate into a sharp increase in prices. However, economics can help us come to terms with this seeming non-sequitur.

A few months ago, I wrote an article on the relationship between oil production, consumption and price - specifically the concept of price elasticity of supply. I plotted oil production (supply) against prices for the period between 2000 and 2010 and got this graph:

")

Elasticity of Global Oil Supply (Source: EIA)

This chart plots production (in mbpd) across the X axis against the price at that production level along the Y axis. This tells us the price elasticity of supply for oil.

In economics, price elasticity is a measure of the extent to which production can increase to meet rising demand. If the supply is elastic, increased production is associated with a very modest increase in price.

")

Elastic supply(Image Credit: Investopedia)

If the supply is inelastic, that means increases in production are accompanied by sharper increases in price.

")

Inelastic supply (Image Credit: Investopedia)

Now look again at the supply elasticity graph for global oil production. As you can see, supply is elastic up to around 83 million barrels per day. It's a classic elastic supply curve.

From 84 mbpd on upward, supply becomes decidedly inelastic, following a classic inelastic supply curve.

This is precisely what peak oil theory predicts: once the production rate peaks, the marginal cost to produce an additional barrel of oil starts racing toward prohibitive.

Last week's oil price spike may appear to have come out of nowhere, but if we take a step back and look at oil production, consumption and price movement over the past few years, we see a pattern emerge.

")

Global daily oil production, consumption and WTI price by month, 2007 to 2011 (Source: EIA)

Particularly over the past year, oil consumption has increased steadily from around 86 million barrels per day (mbpd) in January to 88 mbpd this year. Production has tended to lag behind consumption, and the price started drifting toward $100/barrel in September.

In other words, last week's price spike didn't come out of nowhere after all. It only seems that way because daily journalism has no memory.

Saturday's Spectator editorial warned: "The net result of sustained higher prices for crude oil could be much more serious, and could even push Canada and other countries back into recession."

Unfortunately, the editors seem to think that a stable transition in Libya and increased exports from Saudi Arabia will save the day.

Think again. Saudi Arabia has been promising for several years to assert its traditional role as global swing producer and boost production in response to price signals, and yet its exports continue to decline.

After a June 2008 promise to increase production from 9.5 mbpd to 10 mbpd, Saudi production has actually dropped to 8.5 mbpd in the past two and a half years. Just last December, Saudi oil exports dropped 4.9% in a single month.

Worse still, Saudi exports are falling faster than Saudi production, as domestic consumption increases and diverts a bigger share of the total. This is a general pattern among oil producing countries when they pass their production peaks.

As I warned last May:

Can we replace a two or three percent annual drop in oil production rates through some combination of conserving and replacement without recessionary demand destruction? I'm not so sure.

If we can't, we will spend the next several years reliving the boom-superspike-bust economic cycle again and again, while our indebtedness grows steadily and our median standard of living ratchets down by painful degrees.

And a year before that:

The "bumpy plateau" is what happens when global oil production has reached its maximum rate but demand keeps growing: the price of oil rises, then super-spikes (as Goldman-Sachs termed it in an April 2005 projection) due to a rapid increase in the marginal cost of production until persistent high prices have destroyed enough demand to bring it in balance with supply.

What ends up happening, however, is that the price spikes so high that the economy goes into recession and demand falls significantly below the maximum rate of production. Oil prices collapse in response.

Sooner or later, low oil prices help to spur a new economic expansion, which leads growth in demand for oil until once again it approaches the maximum production rate, leading to another price spike and another economic crisis.

Sound familiar?

This is what we're dealing with: not the temporary blip of a political upheaval or a mercurial despot, but the perpetual squeeze of a market that wants to consume more oil and an industry that simply cannot get oil to market any faster.

At RTH, we've been sounding the alarm about this since early 2005; but even today, it's still nearly impossible to read anything sensible about peak oil in the mainstream news media.

That basic ignorance about what we're dealing with from a macro-economic perspective has devastating consequences.

Council votes to spend billions expanding an airport that will be laughably obsolete in a decade while agonizing over the cost of a new light rail line that will drive urban revitalization and make the city less vulnerable to oil prices.

Suburban councillors fight against narrow frontage and medium-density infill and veto bike lanes - and can't draw the connection between land use that makes car ownership mandatory and suburban drivers crying foul about the rising cost to fill up their SUVs.

Nor will they be able to draw the deeper connection between peak oil and the crippling cycle of economic growth and oil price spikes leading to recession and retrenchment, followed by a slow recovery and another oil price spike.

By highwater (registered) | Posted February 28, 2011 at 11:03:20 in reply to Comment 60374

In related news, it's going down to -12 tonight. Global warming solved!

By SOF (anonymous) | Posted February 28, 2011 at 15:12:14 in reply to Comment 60376

insult spam deleted

By Blinxer (anonymous) | Posted February 28, 2011 at 11:07:17

Highwater loves to come to the aid of embattled editors. The fact of the matter is that both statements of fact are true: it is going down to -12 and oil prices are dropping. Global warming on the other hand is not solved and we are going to see volatility in oil pricing for a long time to come.

We should not wring our hands in Ryan-style desperation though. The end of the world isn't near; and we shouldn't abandon cars and planes because of the facts above. We should innovate, conserve, stabilize geopolitical things and move on.

By geoff's two cents (registered) | Posted February 28, 2011 at 12:21:10 in reply to Comment 60377

I think what is so frustrating about mainstream media coverage of oil price volatility and DoomNGloom's (sadly "common sense") comment is their inability or unwillingness to demonstrate critical thinking skills - i.e. a refusal to consider global warming along the lines of average temperature increases (instead of the "it's snowing outside right now, so global warming must be a farce" approach); as well as a refusal to consider the possibility that long-term habits of oil consumption are generating global economic volatility (instead of the "prices skyrocket when a mere 2% of the world's oil supply is at risk; it must the fault of those idiot speculators" line of argument). Both approaches press into service a mere sliver of available data, and exclude relevant evidence in the interest of a purely self-justifying way of interpreting the world.

Comment edited by geoff's two cents on 2011-02-28 12:22:11

By Borrelli (registered) | Posted February 28, 2011 at 11:34:48

Despite the fact that the Globe has yet to run his column anywhere near a front page, they have been providing space for Jeff Rubin's views on peak-oil for the past couple of years.

http://www.theglobeandmail.com/report-on...

His column and blog, while largely repetitive of arguments he made in his book, is well written, well researched, and very good alternative to the re-heated press releases that we now call "business journalism."

As his bio says (my emphasis),

"The consequences [of rising oil prices] would be severe. He argued that it wasn't sub-prime mortgages, but record oil prices that drove the world economy into its deepest post-war recession. And unless the economy starts to wean itself off an ever depleting supply of affordable oil, he believes there will be other recessions to follow as economic recoveries quickly push oil prices right back into triple digit range. But weaning our economy off oil means some fundamental changes in the way we live.

"That's not the kind of message chief economists' at investment banks are supposed to deliver so he resigned from CIBC World Markets to write about it in his new book Why Your World Is About To Get A Whole Lot Smaller."

Comment edited by Borrelli on 2011-02-28 11:35:15

By RightSaidFred (registered) | Posted February 28, 2011 at 12:10:34

Question for the wiser than I: why are diesel prices now higher than gasoline prices? I bought and drive a diesel Jetta to try and save money. Yes i can go further on a tank of diesel than gas but my point is diesel costs less to refine for public consumption than gasoline. How can the oil companies justify this price descrepancy?

Comment edited by RightSaidFred on 2011-02-28 12:43:54

By Why the resistance? (anonymous) | Posted February 28, 2011 at 13:12:43

Things have to change, however, most people are resistant. They will argue the point to the death. Look around everyone, this system we have created is wrong for many reasons.

Well I guess if oil keeps going up and those in the middle class can no longer afford to pay, then maybe, things will start to change or at least people will be engaged to think about other alternatives.

The consumer driven culture we live in, is completely insane.

By Mr. Meister (anonymous) | Posted February 28, 2011 at 14:12:44 in reply to Comment 60388

What alternative do you propose?

By banned user (anonymous) | Posted February 28, 2011 at 13:38:29

comment from banned user deleted

By Woody10 (registered) | Posted March 02, 2011 at 01:05:20 in reply to Comment 60389

It's not even speculation. It's a pathetic excuse to make more money from us poor, sit on our thumbs, dummies who keep paying and paying, and whining and whining. The government loves it too, look at their increased income from it. Do you think they will do anything on our behalf?? Not bloody likely.

By SOF (anonymous) | Posted February 28, 2011 at 15:14:02 in reply to Comment 60389

insult spam deleted

By Mr. Meister (anonymous) | Posted February 28, 2011 at 14:09:48

Another peak oil piece. How many have you written now? I find it amazing how smart you are and how stupid everyone in the main stream media is.

And then the other day (maybe Friday) Saudi Arabia announced that they were increasing production. That did seem to halt the run up in prices and lead to lower prices.

What infuriates a lot of us drivers is how the gas prices will jump at the slightest increase of crude prices and yet it takes a lot longer to come down when the crude prices drop. It seems when the prices are going up the gas prices rise immediately to compensate for the higher prices to replace the stock. When prices are going down the price cannot drop until the high priced stock in the supply chain is used up.

I am sure that there is a finite amount of oil and we will indeed run out one day. We here in North America are probably better equipped to deal with a rise in gas prices than many other parts of the world.

By mrgrande (registered) | Posted February 28, 2011 at 15:52:38 in reply to Comment 60391

We here in North America are probably better equipped to deal with a rise in gas prices than many other parts of the world.

Why do you say that?

By Mr. Meister (anonymous) | Posted March 01, 2011 at 15:09:55 in reply to Comment 60408

Our gas prices are among the lowest in the world especially compared to Europe. We produce a lot of crude oil. As the price of crude goes up more of the fringe oil starts to become financially feasible which will help our economy. We tend to have a higher disposable income than some other parts of the world like India, China and some others.

How would you like to be in France be paying $2.50 for a liter of gas and hear that the price is doubling?

By Brandon (registered) | Posted March 01, 2011 at 15:16:19 in reply to Comment 60464

Seeing as the vast majority of the European prices are taxes, the gov't there has far more room to play to keep things level if they want to.

By A Smith (anonymous) | Posted February 28, 2011 at 14:41:02

From 1946-1971, the U.S was on the gold standard and oil prices stayed between $18-$24 U.S./barrel, after adjusting for inflation. Look at what happened after Nixon left the gold standard in 1971...

http://goldprice.org/images/monthly_dollar.gif

Curiously enough, that's when the price of oil took off, climbing 400% (inflation adjusted) in less than 10 years (tinyurl.com/67rwxeu)

Back to the gold chart, notice that between 1981-2004, gold prices stayed relatively flat. During that same period of time, oil remained flat as well, around $30/ barrel.

Here is the price of other items in U.S dollars, notice the jump after 2004...

http://www.indexmundi.com/commodities/?commodity=copper&months=300

http://www.indexmundi.com/commodities/?commodity=tea&months=300

http://www.indexmundi.com/commodities/?commodity=cocoa-beans&months=300

http://www.indexmundi.com/commodities/?commodity=wheat&months=300

http://www.indexmundi.com/commodities/?commodity=sugar&months=300

http://www.indexmundi.com/commodities/?commodity=oranges&months=300

http://www.indexmundi.com/commodities/?commodity=soybeans&months=300

http://www.indexmundi.com/commodities/?commodity=rubber&months=300

http://www.indexmundi.com/commodities/?commodity=cold-rolled-steel&months=300

http://www.indexmundi.com/commodities/?commodity=steel-wire-rod&months=300

By JonC (registered) | Posted March 01, 2011 at 18:11:06 in reply to Comment 60395

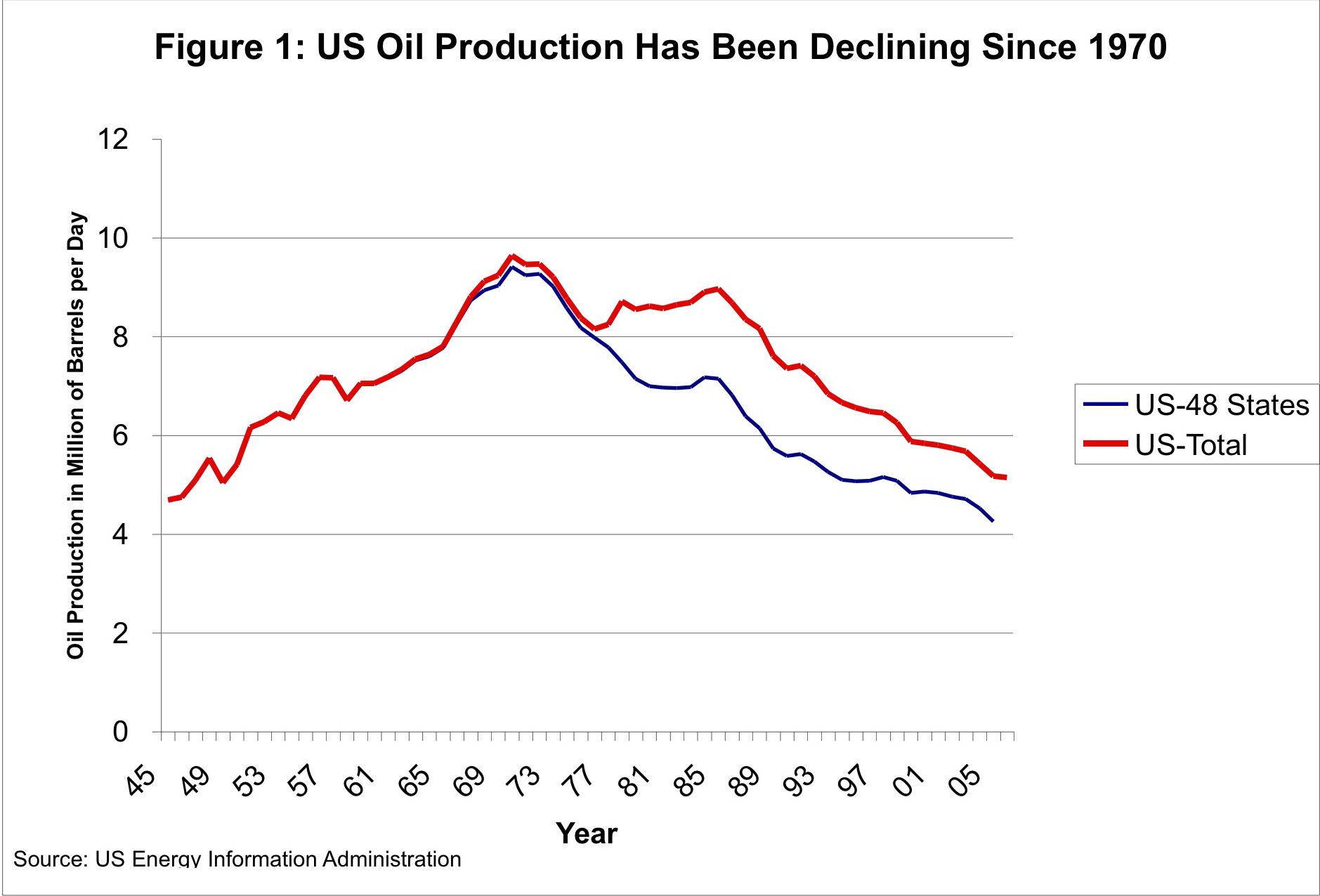

Or, it was US peak oil. When you start needing more than you produce you lose control over pricing. http://en.wikipedia.org/wiki/File:US_Oil...

By Why the resistance (anonymous) | Posted February 28, 2011 at 14:49:35

Mr Meister: I think what needs to happen is that honest dialogue and discussion about our insane consumer driven society. People do need to rethink things, the current system in place is destroying the environment, it leaves behind many people, large amounts of poverty, people keep buying crap, that they do not need. In my mind I ask, who and what gives the business elite the right to direct things or that we should just accept what they want when the business elite do not exactly act in the benefit of all people.

I just took a class Labour and Media and watched a film, Class Dismissed which brought into focus the role that advertisers played in the shaping of TV. Since the earlier 1950's we have all been barraged with consumer goods, that gave and still gives the supposed picture of a good living standard. Everything that is manufactured, is under the guise of planned obsolence, meaning, the product will break down rather quickly, which in turn fills landfills with waste. How many people out there today, have consumer debt, large amounts, just in their quest to keep up with the Jones.

Should we as a society base our success on the number of consumer products we have or should be about something else, the common good of all society and members of the human race across the globe. How about mother nature and all its creatures.

Should not our focus be on ensuring the every member of society has shelter, food, clean water. We are and have always been in a class war, when maybe the refocus should engage all workers and people to acknowledge that things are wrong and if we do not join together to have our voices heard, we can all be losers at some point in the future.

People like yourself are stuck in a mode and will not allow for some honest reflection. Please think about what we are all leaving behind for our grandchildren and beyond.

What affects one, affects us all!

By jasonaallen (registered) - website | Posted February 28, 2011 at 15:38:07

I have always said that people don't come to conclusions about 'big ticket' items (such as Capital Punishment, Left vs. Right politics, Gay Marriage, Climate Change etc) based on a logical review of the facts, and a carefully thought out decision-making process.

They make an emotional decision, and then scramble to find the 'facts' to back it up.

In the end, I think one thing the Transition movement does well is understand that it's not graphs and charts and figures that will convince people, it's a good narrative, and putting everyday experience into the big picture context of what we are undoubtedly living through.

For some, though, even the good narrative won't be enough, which is no reason to give up trying to get the message across to those who will listen. 10 years ago, Peak Oil was the domain of a lunatic fringe, but as more people opened their eyes to what was really going on, it has become more and more accepted.

In the end, I think RTH is on the right track in terms of a slow and steady banging of the drum.

By spicate (anonymous) | Posted February 28, 2011 at 15:52:02

All the people on here denying that there is a problem should try asking themselves where the additional production we need is going to come from.

By banned user (anonymous) | Posted February 28, 2011 at 15:58:14

comment from banned user deleted

By JonC (registered) | Posted March 01, 2011 at 18:22:51 in reply to Comment 60409

While the oil sands have reduced a gap between consumption and production, it has increased total consumption. That's entropy. Unless oil can by synthesized using less energy that it would produce (some sort of passive procedure, of which there are currently none) we are constantly running out. To think otherwise is folly. Any sort of efficiency just draws out the process.

It doesn't matter how fast the car is going, it's stopping when it hits that wall.

By banned user (anonymous) | Posted March 01, 2011 at 18:43:02 in reply to Comment 60474

comment from banned user deleted

By JonC (registered) | Posted March 02, 2011 at 17:06:28 in reply to Comment 60476

I didn't question a net production, I question your statement that there is a reduction in cosumption. Even just using those numbers one would need to extract three times as much as a "clean" source of oil, thereby consuming more energy. You've also done nothing to argue the fact that you're running out of oil. All you did was argue something completely different.

By banned user (anonymous) | Posted March 03, 2011 at 09:49:28 in reply to Comment 60603

comment from banned user deleted

By JonC (registered) | Posted March 03, 2011 at 11:45:03 in reply to Comment 60652

"the oil sands for one, stabilized consumption, perhaps even reduced consumption"

By banned user (anonymous) | Posted March 03, 2011 at 11:49:41 in reply to Comment 60666

comment from banned user deleted

By JonC (registered) | Posted March 04, 2011 at 07:05:35 in reply to Comment 60667

"I didn't say that there was a reduction in consumption" -say what, March 3rd

"the oil sands for one, stabilized consumption, perhaps even reduced consumption" -say what, March 1st

Comment edited by JonC on 2011-03-04 07:06:58

By banned user (anonymous) | Posted March 04, 2011 at 07:33:45 in reply to Comment 60686

comment from banned user deleted

By A Smith (anonymous) | Posted March 02, 2011 at 17:10:09 in reply to Comment 60603

Could you please name one resource that humans have ever run out of.

By JonC (registered) | Posted March 03, 2011 at 11:49:46 in reply to Comment 60604

By Tybalt (registered) | Posted March 02, 2011 at 22:01:54 in reply to Comment 60604

Vast numbers of animal and plant species have gone extinct via human intervention, many through consumption. Hell, we nearly lost the goddamn bison, one of the greatest natural resources of this continent.

Very many human populations have lost almost their entire resource base (agricultural land, building materials, animal resources, everything) due to human intervention. Easter Island is one, Anasazi seems to be another, there are many many more examples. The story of populations catastrophically running out of resources is as old as the species.

By A Smith (anonymous) | Posted March 03, 2011 at 00:10:33 in reply to Comment 60623

>> Very many human populations have lost almost their entire resource base (agricultural land, building materials, animal resources, everything) due to human intervention.

Sure, and in how many of those societies did they respect private property rights and use market prices to allocate resources?

Think about why the 407 doesn't have traffic jams, while the 401 does, or why there are plenty of laser eye clinics, but a shortage of family doctors. In both cases, the market based provider never runs out of goods/services, only the government manages to do that.

By Tybalt (registered) | Posted March 03, 2011 at 08:06:32 in reply to Comment 60633

Are you even listening? We killed off the bison, to take one example, and ended it as a resource precisely because of the efficiency of the unregulated market.

By A Smith (anonymous) | Posted March 03, 2011 at 10:13:00 in reply to Comment 60642

Here is a quote from wikipedia that explains the bison depletion...

"The US Army sanctioned and actively endorsed the wholesale slaughter of bison herds.[28] The US federal government promoted bison hunting for various reasons, to allow ranchers to range their cattle without competition from other bovines, and PRIMARILY to weaken the North American Indian population by removing their main food source and to pressure them onto the reservations.[29] Without the bison, native people of the plains were forced either to leave the land or starve to death.

...

If these bison has been located on private land, what jurisdiction would the US government have had in promoting their slaughter?

By drb (registered) - website | Posted March 03, 2011 at 01:39:30 in reply to Comment 60633

Come on Smith. Enough with the bait and switch. Your first response was with regard to resources. I admit if your are talking about natural resources we haven't run out of any yet. But other than solar based resources (agriculture, energy), or geothermal energy most other natural resources are finite, either by supply or the economics of extraction. The Earth simply cannot resupply these resources given the speed of our consumption.

Highways, laser eye clinics, and any other market based "resource" rely entirely on finite natural resources. They are Products not resources! You can't pick and choose which part of the economy you use to make your point.

Purposefully misrepresenting products as resources is dishonest and an unfair response to Tybalt's answer to your question.

By A Smith (anonymous) | Posted March 03, 2011 at 11:15:43 in reply to Comment 60635

drb >> Purposefully misrepresenting products as resources is dishonest and an unfair response to Tybalt's answer to your question.

I was trying to highlight an apples vs apples comparison (similar products, roads, health care) under two different allocation methods, free market prices vs government handouts.

In both cases, shortages are only produced when prices are not used as the method of allocation.

As long as anything (resources, consumer goods) that people buy is priced to match supply and demand, shortages will be short lived and rare.

Take jewelery for example. It's in very high demand amongst the female crowd and yet there are no shortages. This is not because there is a large supply of fine stones in the world, it's because they are allowed to be bought and sold at a price.

By highwater (registered) | Posted March 03, 2011 at 10:22:53 in reply to Comment 60635

Purposefully misrepresenting products as resources is dishonest and an unfair response to Tybalt's answer to your question.

and A Smith's MO.

Heed Ryan's warning and get out while you still can.

By z jones (registered) | Posted March 02, 2011 at 18:14:57 in reply to Comment 60604

Patience with your incessant trolling.

By Undustrial (registered) - website | Posted February 28, 2011 at 16:21:46

The economic ignorance displayed in the whole "speculation" argument really blows me away. It's as if nobody's seen speculation before. We live in a capitalist society - what commodity's price isn't regularly inflated by speculation? Furthermore, the notion that a 2% drop in supply shouldn't generate much more than a 2% increase in price is similarly absurd. That's just not how supply and demand work.

The constant flood of stories which claim to "disprove" peak oil by pointing to side effects are simply dishonest. There's a point beyond which it's not an act of "keeping people calm" and instead it's just perpetuating a crisis. It's very fashionable to be a "skeptic" and to dismiss "doom-sayers" these days. Unfortunately, fashion isn't logic, and denial doesn't solve problems.

By A Smith (anonymous) | Posted February 28, 2011 at 16:51:50

Copper was up by more 433% from Jan 2001- Jan 2011. In that same period of time, oil was up only 257%.

Coal is up 341% from Jan 2001- Jan 2011...

http://www.indexmundi.com/commodities/?commodity=coal-australian&months=120

U.S coal prices are up 125% from 2000-2009 in a poor economic time period. From 1981-2000, in a good economic time period, they dropped 25%.

In 2006, world coal consumption was 3.09 billion tonnes. At that rate of consumption, the world has 287 years of proven coal reserves. And yet coal prices keep going up just as oil prices go up.

It's not just oil, it's everything that is seeing price increases. This doesn't prove we are running out of everything, it proves that the Fed is printing too many pieces of paper. Even Alan Greenspan is saying a move to a gold standard would be helpful to reduce prices...

http://www.youtube.com/watch?v=z5MVsm2cpc0

By Tybalt (registered) | Posted March 02, 2011 at 01:37:17 in reply to Comment 60411

I would no more trust Alan Greenspan to tell me about economics than I would trust him to drop a 454 into a '73 Chevelle without getting grease on his wingtips.

By mikeonthemountain (registered) | Posted March 01, 2011 at 12:34:29 in reply to Comment 60411

Actually we are running out of everything.

http://www.newscientist.com/data/images/...

Wasteful consumption will be mitigated by choice or by math i.e. physical reality. The clock is ticking on the choice part.

By JasonAAllen (registered) - website | Posted February 28, 2011 at 21:17:06 in reply to Comment 60411

I don't think anybody is claiming that the high price of oil is (the only) proof that oil is running out. We have geology for that. http://en.wikipedia.org/wiki/Hubbert_cur...

By A Smith (anonymous) | Posted February 28, 2011 at 17:21:38

If the U.S. were still on the gold standard, this is what gas prices would be...

http://pricedingold.com/us-retail-gasoline/

As you can see, gas prices are not high because there is a shortage of gas relative to gold, they're high because there is a shortage of gas relative to U.S dollars created by the Fed.

By JasonAAllen (registered) - website | Posted February 28, 2011 at 21:31:32 in reply to Comment 60413

No... oil prices are high because the bottom sludge they are pulling out of the tar sands, or the light sweet crude they are drilling 3 miles below the ocean floor off the coast of Brazil is considerably more expensive to get at - AND because the cheap/easy to get to/easy to refine oil is now in decline - at least according to the International Energy Agency. The price of oil has nothing to do with monetary supply, but rather...wait for it...oil supply. There simply isn't enough cheap/easy to refine oil left to satisfy world demand at a price that will enable the economy to grow in an unfettered way.

Why is that so hard to understand?

The Earth stopped making oil several hundred million years ago. We currently use 86 million barrels a day. That's almost 15 billion litres a day. Doesn't it stand to reason that if we pull that much oil out, and production stopped 100 million years ago, that sooner or later we're going to run out? And now ALL of the geological evidence is pointing to just that fact?

I know what we're going to be facing is not going to be fun, but the arguments against Peak Oil at this point amount to little more than someone with their hands over their ears shouting "LA! LA! LA I can't hear you!" Frankly, I find it baffling.

By A Smith (anonymous) | Posted March 01, 2011 at 00:10:13 in reply to Comment 60430

Jason Allen >> The price of oil has nothing to do with monetary supply, but rather...wait for it...oil supply.

Here is a chart that prices oil in grams of gold...

http://pricedingold.com/crude-oil/

In 1950, it took 2 grams of gold to purchase 1 barrel of oil. As of February 8, 2011, it took two grams of gold to buy 1 barrel of oil.

What does this tell us? It tells us that the increase in the nominal price of oil is entirely the result of too many U.S. dollars being produced.

>> There simply isn't enough cheap/easy to refine oil left to satisfy world demand at a price that will enable the economy to grow in an unfettered way.

According to the EIA...

http://www.eia.doe.gov/aer/txt/ptb1105.html

world oil production remained flat from 1979-1996. In that period of time, oil prices, as measured in gold fell from approximately 2.5 grams per barrel to 1.5 grams per barrel.

Also, in that same period of time, production worker's hourly wages, as priced in grams of gold went from 0.50 an hour to 1.00 an hour.

By Tybalt (registered) | Posted March 02, 2011 at 01:45:09 in reply to Comment 60437

This is a dandy thought, except that (1) we are also running out of gold. (We are not, of course, running out of dollars, far from it). The way you price one intensively mined commodity is not in relation to another intensively mined commodity.

Also, (2) during the last major contraction of energy supply, gold prices also surged dramatically. There is every reason to believe - based on both historical data and investment models - that people will retreat in greater numbers to stable retainers of value gold when energy prices (and therefore business operating expenditures) increase.

Obviously, the point that is being made is that oil is costing more, relatively, than other goods when priced against those same dollars, ounces of gold, and what have you.

You seem to know just enough economics to be dangerous to yourself, kid. I encourage you to learn some more.

By mrjanitor (registered) | Posted February 28, 2011 at 17:54:36

In 1956 an educational movie called Our Mr. Sun was produced and talked about how we were going to run out of energy. For the impatient please watch from 42:15 to 45:00. Energy is discussed until the end, where the consequences of not using solar power are shown from 51:00 to 51:29. The term 'peak oil' was not invented yet but it's coming was clearly alluded to in the movie. It's produced by Frank Capra so it gets a little preachy but it's worth watching the whole movie to see what scientists were thinking of in the mid 50's.

I also remember seeing another old movie (old even then) when I was in school around 1974 that also talked about running out of energy in 50 years or so, can't find that one on the internet yet but I'll keep looking.

By A Smith (anonymous) | Posted February 28, 2011 at 18:28:38

Take a look at this chart measuring U.S. GDP in gold, rather than paper currency. Notice that during both the seventies and the 2000's, GDP as measured in gold fell, most people became unhappy with the economy and their leaders.

Conversely, in the times when GDP as measured in gold went up, people were happier and optimistic.

It's not complicated, if you want a good economy, you need to use real money, not IOU's from the government.

By Tybalt (registered) | Posted March 02, 2011 at 01:48:53 in reply to Comment 60419

This gold nonsense is, well, nonsense. Gold is a medium of exchange with no more intrinsic worth than greenbacks (except for its applications in industry, dentistry, etc. but then I can also stuff a duvet with dollars) Its relatively stable ability to preserve value arises from the fact it's shiny and hard to dig up from the ground, and from the fact that it has a longer cultural resonance than notes do.

By JonC (registered) | Posted March 01, 2011 at 18:34:52 in reply to Comment 60419

So your current argument is that the economy is sustained by happiness. You have outdone yourself. Kudos.

By A Smith (anonymous) | Posted February 28, 2011 at 18:29:17 in reply to Comment 60419

Here is the chart...

http://pricedingold.com/us-gdp/

By mrjanitor (registered) | Posted February 28, 2011 at 18:29:41

Here is another one from 1958 which discusses carbon emissions and global warming. It's only a short clip.

By Undustrial (registered) - website | Posted February 28, 2011 at 20:54:19

As much as I don't particularly think a return to the gold standard is a solution, A Smith is onto something with many of his points.

a) The Gold Standard. Abandoned in the early 1970s so the US government could print more money to finance the Vietnam War, this had huge effects on the world's economies. Around this same time American oil peaked and mideast tensions (once again) came to a head, leading to round of oil embargoes which quickly created the oil crisis. What this all meant was that countries like Iraq and Saudi Arabia suddenly found themselves with enormous amounts of captital, and started investing it - usually in regions like Sub-Saharan Africa. This is the primary root of today's third world debt crisis. A fascinating topic to be sure.

b) Oil is not the only commodity price going up. This suggests, without a doubt, that there's some common causes (ie: speculation, etc), but also something far more frightening: oil is not the only resource running out. Not really surprising given that most uses for oil also involve copious amounts of water, metals, land etc. And much like oil - it isn't that they're vanishing altogether - simply becoming harder to economically extract in useful forms. We'll probably never run out water we could drown in - but we're rapidly running out of water we can drink or water crops with. Check out Richard Heinberg's "Peak Everything" for more info.

c) Even if there is a real basis for rising oil prices, it's taking place in an utterly absurd economic context. And while I might argue that such a context was able to keep oil prices artificially low for most of the last few decades - it's now doing the exact opposite. If a 2% drop in supply can jump prices by 20-30%, then what can we expect from a sustained 10% drop? Our society needs to take a really serious look at why we're so willing to print billions of dollars of make-believe money because the people we give it to tell us it's good for us.

By Myrcurial (registered) - website | Posted March 01, 2011 at 13:14:53

Ryan - I am deeply offended by your sweeping statements. Not all despots are Myrcurial. Primarily due to the fact that I am not a despot. But it seems to be a good job for about 20 years or so.

Also, great article - but as I'm often accused of - pointing at a problem without also pointing at a set of solutions ranging from managable to bat-5h!7 crazy.

:)

*EDITED TO ADD: the potential upside of being a despot.

Comment edited by Myrcurial on 2011-03-01 13:15:34

By TnT (registered) | Posted March 01, 2011 at 14:07:03

What about the use of Natural Gas, Ethanol, electric to keep the cars on the roads? How do we adapt?

By BobInnes (registered) - website | Posted March 01, 2011 at 15:24:49

Great debate! Everybody has a point, even the naysayers and monetarists. A.Smith's data is interesting indeed. I remember hearing somewhere that during the runup in o8, every tank, tanker and bathtub that could hold oil, did. To the point that the Baltic index showed both the tightening of ship supply and the subsequent unwinding. Ryan is writing about his longer term bet in a way that smooths the graph. It is surprising how long the long term is taking, which is the cynics' point. As traders say, Mr Market (the trend) can continue longer than you/we can remain solvent (in our bets). GLTA

By Shempatolla (registered) - website | Posted March 02, 2011 at 19:34:58

Ummm a little quick math and I will state, I'm no statistician, but adjusted for inflation, gas is roughly the same price it was 30 years ago. Meaning as a percentage of our disposable income, it doesnt cost us any more. Other things like housing, food, education, health care, have all risen drastically compared to the price of gas.

By Tybalt (registered) | Posted March 02, 2011 at 22:10:32 in reply to Comment 60614

Hey, everyone, let's play selective endpoints!

You picked the exact moment when gas prices were at an all-time high (an all-time high, that is, until 2008) as the start endpoint for your price comparison? That, sir, is a remarkable piece of mistake engineering.

I'd note that the period around 1981 represents the last time a significant constricting pressure existed on the gasoline supply - it is the source of the stories about gas shortages we were just hearing so much about.

(We usually associate that with "the 70s" but just as most of "the 60s" happened in the 70s, most of "the 70s" happened in the 80s. I digress :)

So since the only other time comparable dollar-stable prices for gasoline existed, was the period around 1981, I'd say you just succeeded in supporting the exact opposite point to the one you thought you were.

Hard luck, old sport.

By hammertime (registered) | Posted March 03, 2011 at 07:59:20

What oil shortage? The US continues to buy up oil from all over the world while they sit on untapped reserves.

By Tybalt (registered) | Posted March 03, 2011 at 08:11:21 in reply to Comment 60641

Sure; now since we're all being such smart, practical economists here, I'll point out to you that the cost of extracting a resource (which is what we are talking about here, remember) includes all the political costs associated with extracting it. If resources are locked away for political reasons.

If we can't get at that oil because political forces mean we can't tap it, then guess what, it doesn't help deal with the production shortage. Remember, the issue with a "shortage" is only that oil is becoming more costly to extract, not that we're going to suck the well dry in five years.

All the remaining US oil reserves are high-cost-of-extraction anyway. There are now low-cost reserves left.

By Undustrial (registered) - website | Posted March 03, 2011 at 12:35:29

The 'Oil Shocks' of decades past happened to fall right after the peak of American oil extraction in about 1970. A similar embargo was tried in 1967, but had little effect as Texas simply pumped more. In 1973 that the peak had been slightly passed, the economics of that were all different, and gas lines formed. For all of America's money and technology, it's seen a constant fall in lower-48 production since about 1970.

http://gailtheactuary.files.wordpress.co...

We need to be really careful what we deem simply "political" reasons for oil shortages. Actual oil shortages underlie many large-scale political events (see the theories of a peak shortly before the fall of the USSR), as well as economic ones. More importantly, though, it raises some serious questions about how we see "oil" globally. If Saudi Arabia decides to cut back on oil production in order to raise prices, is that necessarily an attack on US and OUR oil supplies?

The single dumbest thing Saudi Arabia could be doing right now is pumping all of their easily accessible oil as fast as possible. Doing it with the conscious purpose of lowering global oil prices is doubly stupid. It ensures not only that they'll have little oil to sell in the future (when prices are likely far higher), but it does everything possible to shrink their income per barrel in the present. Would choosing to act differently - a responsible and conservative approach which slowed production to ensure some in years to come - be a "conspiracy" against us? Something to punish with wars, sanctions or the installation of (another) puppet government?

To put it another way, do I have the right to siphon my neighbour's gas if I don't want to pay his asking price? Is it simply a "political" decision to not allow me to do so?

By hammertime (registered) | Posted March 03, 2011 at 20:07:30

Sarah the nut job has the answer. Drill baby drill.

By Mogadon Megalodon (anonymous) | Posted May 19, 2011 at 13:15:46

http://www.youtube.com/watch?v=I8D_j9fqfUg

You must be logged in to comment.

There are no upcoming events right now.

Why not post one?

{kind=link}

{kind=link}

{kind=link}